Forex Trading Tax in Nigeria: FIRS, PITA Rates and How to Declare

Here is the question every Nigerian trader eventually asks, usually after their first profitable month: do I actually have to pay tax on this?

Yes. And the rules are more straightforward than most traders expect, because Nigeria already has a framework that captures forex trading profits without needing a dedicated statute. The Personal Income Tax Act Cap P8 LFN 2011 (PITA) treats forex trading income the same way it treats any other business or trading activity.

This guide explains how the Federal Inland Revenue Service (FIRS) taxes forex trading profits, which rates apply, how to file correctly, and what records to keep. For a broader overview of how forex trading in Nigeria works before getting into the tax treatment, that pillar covers the mechanics in full.

Is Forex Trading Income Taxable in Nigeria?

Yes. Forex trading profits earned by Nigerian residents are taxable under PITA. The Act taxes income derived from trade, business, or a profession regardless of whether the activity is carried out through a foreign broker or a local one. Nigerian tax residents are liable on their worldwide income, so profits sitting in an offshore account are not exempt.

The taxing authority depends on your employment status and state of residence. Salaried employees are taxed through the Pay-As-You-Earn (PAYE) system administered by the State Internal Revenue Board (SIRB) of the state where they are domiciled. Self-employed traders and sole proprietors file with FIRS if they operate as a business, or with their state SIRB if they earn income as individuals.

What counts as forex trading income under PITA?

PITA treats forex trading profits as income from a trade or business when the activity is carried on with a view to profit and with regularity and system. In practice, this means:

Profits from speculative trades (buying and selling currency pairs for capital gain)

Swap income and rollover credits received on open positions

Bonuses or rebates paid by brokers that constitute income in your hands

Losses from forex trading may be set off against other income from the same source in the same year of assessment, or carried forward against future forex profits, subject to FIRS guidelines.

What about capital gains tax?

The Capital Gains Tax Act (CGTA) imposes a 10% tax on chargeable gains from the disposal of chargeable assets. Foreign currency held as an investment asset can in principle constitute a chargeable asset. However, FIRS administrative practice and the predominant legal view treat actively traded forex accounts as a trading activity rather than a capital asset disposal. Most Nigerian tax practitioners file active forex profits under PITA as trading income rather than under the CGTA as capital gains. If your activity is infrequent or you hold currency positions over extended periods as a store of value, a CGTA analysis may be warranted. Obtain independent tax advice for your specific circumstances.

Is forex trading tax-free in Nigeria?

There is no statutory exemption for forex trading profits under Nigerian tax law. Claims that retail forex income is automatically tax-free because it is earned offshore or through a foreign broker have no basis in PITA. The fact that your broker is based outside Nigeria does not extinguish your Nigerian tax obligation.

The information in this section is general in nature and reflects the legislation and FIRS administrative guidance available as at the date of publication. Tax law and its interpretation can change. Consult a qualified Nigerian tax adviser before filing a return that includes forex trading income.

How PITA Classifies Forex Trading Income

PITA does not name "forex trading" as a specific income category. Classification depends on the nature of your activity, and that distinction determines both your tax rate and what you can do with losses.

Trading as a business. If you trade forex consistently, systematically, and with the intention of profit, FIRS treats the activity as a trade or business. The net profits are assessable income under Section 3 of PITA, taxed alongside your other chargeable income for the year. This is the classification that applies to most active retail traders.

Speculative gains. If your trading is occasional and lacks the hallmarks of a regular trade, FIRS may characterise the gains as speculative. Speculative income is still chargeable to tax under PITA -- Nigeria does not exempt it -- but losses from speculative activity cannot be offset against income from other sources. They carry forward and can only be set off against speculative profits in future years.

Capital gains treatment. The Capital Gains Tax Act (Cap C1 LFN 2004) imposes a flat 10% charge on gains from the disposal of chargeable assets. Currency itself is not listed as a chargeable asset under the Act, which means straightforward forex trading profits are not subject to CGT and instead fall within PITA's income tax framework. If you hold forex-denominated instruments that could be construed as assets, FIRS may take a different view, and professional advice is warranted.

For most Nigerian retail traders operating through a standard forex account, business income classification under PITA is the applicable framework.

Nigerian Personal Income Tax Rates Applicable to Forex Profits

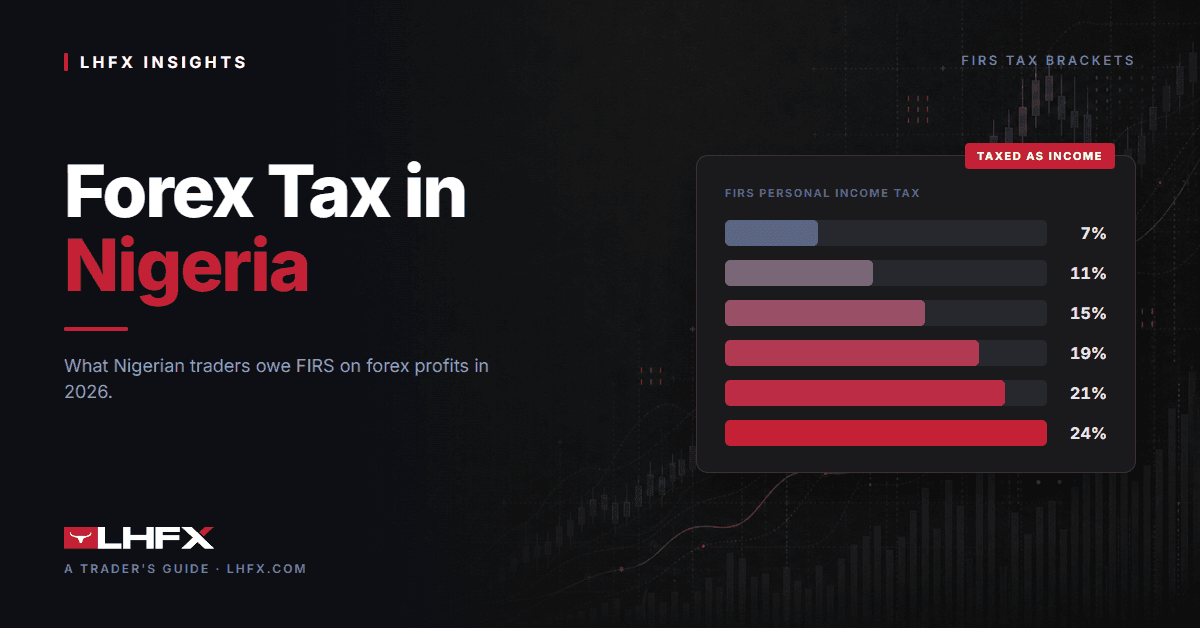

Once your forex profits are classified as chargeable income, they are added to your total annual income and taxed on a graduated scale under the Seventh Schedule to PITA. The forex trading tax rate in Nigeria is not a flat figure -- it depends on where your total income falls across these bands:

Annual chargeable income (NGN) | Rate |

|---|---|

First 300,000 | 7% |

Next 300,000 | 11% |

Next 500,000 | 15% |

Next 500,000 | 19% |

Next 1,600,000 | 21% |

Above 3,200,000 | 24% |

These bands apply to your total chargeable income. Your forex profits do not sit in a separate bucket. If you also earn a salary, consulting fees, or rental income, all of it aggregates before the bands are applied. Forex profits that push you from one band into the next attract the higher marginal rate only on the portion that crosses the threshold.

Available reliefs and deductions. Chargeable income is not the same as gross profit. Before the bands apply, PITA allows several deductions:

Consolidated Relief Allowance (CRA): The higher of NGN 200,000 or 1% of gross income, plus 20% of gross income. This is deducted automatically and reduces the taxable base meaningfully at lower income levels.

Pension contributions: Contributions to a pension fund registered under the Pension Reform Act are deductible up to 8% of monthly emoluments.

Business expenses: For traders assessed under the business income category, costs directly and wholly incurred in generating the trading income -- including VPS costs, data subscriptions, and software licences -- are deductible. Personal expenses and capital items are not.

The minimum tax provision. PITA includes a minimum tax rule that prevents taxpayers from reporting zero liability through deductions and reliefs. Where your tax liability after reliefs falls below 1% of your gross income, you are assessed at 1% of gross income instead. For a forex trader whose gross income is largely trading profit, this provision sets a floor on what FIRS will accept as your annual liability.

Practical implication of the carry-forward rule. A losing year is not a dead year for tax purposes. If you net a loss of NGN 500,000 from speculative forex trading in a given year, record it on your Form A self-assessment return for that year. When the following year produces a profit, you apply the carried loss first and pay tax only on the net. This requires clean, year-by-year records: broker statements, deposit and withdrawal logs, and the exchange rates used to convert USD profits to naira. Without documented losses on a prior return, FIRS will not accept the carry-forward claim.

How to Declare Forex Trading Profits to FIRS

Once you have calculated your net forex income for the year, the next step is filing it correctly with FIRS or your state Internal Revenue Board (IRB). The process follows five steps.

Step 1: Register for a Tax Identification Number (TIN)

If you do not already have one, register for a TIN at any FIRS office or through the Joint Tax Board portal. You cannot file a return without it.

Step 2: Gather your trading records

Compile all documentation that supports your income figure: broker statements, bank receipts showing naira conversions, screenshots of platform transaction histories, and any records of losses you intend to offset. FIRS requires you to retain these records for a minimum of six years from the relevant assessment year.

Step 3: File on TaxPro-Max

FIRS processes individual income tax returns through its TaxPro-Max platform. Log in with your TIN, select "Self Assessment," and enter your total forex income in the appropriate income line. If you have deductible losses from prior years, record them in the designated loss carry-forward field.

Step 4: Meet the 31 March deadline

The annual self-assessment return for the preceding year is due by 31 March. Filing after this date triggers a late-filing penalty of NGN 25,000 per return for individuals. Interest on unpaid tax accrues at the prevailing CBN monetary policy rate plus 10 percentage points, calculated from the date the tax became due.

Step 5: Pay and keep proof

After submitting the return, generate a payment reference on TaxPro-Max and settle the balance through any FIRS-approved payment channel. Save the payment confirmation alongside your trading records -- both must be producible within the six-year retention window if FIRS raises an inquiry.

A note on state IRBs. If you are a salaried employee who also trades forex, your employer remits PAYE on your employment income, but forex profits earned outside that employment are a separate assessable income. Declare them on your individual self-assessment return. Residents of Lagos file with the Lagos Internal Revenue Service (LIRS); residents of other states file with their respective state IRBs.

Record-Keeping Requirements for Forex Traders in Nigeria

Accurate records are not optional for Nigerian forex traders -- they are the legal foundation of every tax return you file. Without them, FIRS can invoke Section 54 of PITA and raise a best-of-judgment assessment: the agency estimates your income and issues a bill you must pay unless you can disprove it. That almost always means a larger liability than your actual profits.

What to keep. Retain the following for every trade you execute:

Trade confirmations: the entry date, exit date, currency pair, lot size, opening price, and closing price from your broker's statement.

Account statements: monthly or annual summaries downloaded directly from your broker's platform, showing all deposits, withdrawals, swaps, and commissions.

Bank and wallet records: evidence of every NGN withdrawal you receive, including the bank credit alert, transfer receipt, or e-wallet transaction log.

CBN exchange rates: the official CBN rate on the date each profit was repatriated or converted. You will need this to translate USD (or other foreign currency) profits into naira for tax purposes.

Expense receipts: VPS subscriptions, charting software licences, and trading education costs you intend to claim as deductions.

How long to keep records. Nigerian tax law requires you to retain business and income records for a minimum of six years from the end of the relevant tax year. FIRS audits are not time-barred within that window.

Converting foreign currency profits to naira. FIRS requires income to be declared in naira. Use the CBN's published rate on the date you received or realised the profit -- not the parallel market rate and not an average. A simple trade ledger with columns for date, currency pair, lot size, profit or loss in USD, the CBN rate applied, and the naira equivalent satisfies the documentation standard FIRS expects and keeps you audit-ready throughout the retention period.

Can Forex Trading Losses Offset Other Income in Nigeria?

It depends entirely on how your forex income is classified, and the rules diverge sharply once you know where the loss sits.

If your forex activity is treated as a trade or business, your net loss for the year is generally deductible against other income under Section 20 of PITA. A trader who netted an NGN 500,000 forex loss and received NGN 1,200,000 in salary during the same year would report NGN 700,000 as assessable income, not NGN 1,200,000.

Losses that cannot be fully absorbed in the current year may be carried forward and offset against profits from the same trade in future years. There is no statutory limit on the number of years a trade loss can be carried forward under PITA, though the loss must be kept alive by filing returns that formally claim it each year.

If your forex activity is treated as speculative income, Section 3(2)(c) of PITA includes speculative transactions as a source of taxable income, and FIRS guidance treats losses from such transactions as offsettable only against future speculative gains from the same activity -- not against salary or other income sources.

If your forex activity is treated as investment income, losses sit in a separate silo and can only shelter future gains of the same character, if any arise.

The practical dividing line is whether FIRS regards you as carrying on a trade. Frequency of transactions, use of leverage, active management, and dependence on the income as a livelihood are all factors. A trader placing dozens of positions a week on a leveraged account is unlikely to be classified as a passive investor.

Before filing a return that claims a forex loss as a deduction against other income, confirm in writing with a tax adviser or your state IRB which category your trading falls into. Filing a deduction in the wrong category is the kind of error FIRS assessments are built to catch.

When to Consult a Nigerian Tax Practitioner

Most forex traders in Nigeria can file a straightforward PITA return without professional help once they understand the framework. There are four situations where engaging a chartered tax practitioner is worth the cost.

Your trading spans multiple income sources. If forex profits sit alongside employment income, rental income, or business income, the interaction between state and federal obligations becomes non-trivial. A practitioner maps each income stream to the correct authority and avoids double declarations.

You have unresolved prior years. FIRS can assess back taxes for up to six years under PITA. If you have been trading and not filing, a practitioner can negotiate a voluntary disclosure arrangement before an audit forces the issue.

Your records are incomplete or inconsistent. Before your first appointment, pull full account statements from your broker covering every closed trade in the assessment year, including per-trade commission figures. If your broker charges $3/side, that cost is deductible against gross gains and must appear line-by-line in the statement. MT4 and MT5 platforms both export this detail natively.

You received a FIRS query or notice of assessment. Do not respond to a formal FIRS query without a practitioner reviewing the notice first. The response window is typically 30 days and the wording of your reply affects your position in any subsequent objection proceedings.

To find a qualified practitioner, look for membership of the Chartered Institute of Taxation of Nigeria (CITN). CITN members are bound by a professional code and are recognised by FIRS.

LHFX: A Regulated Broker for Nigerian Forex Traders

LHFX does not withhold tax on withdrawals and does not report trading activity to FIRS on your behalf. Declaring profits is your responsibility, every year.

A few platform features that make the record-keeping easier:

MT5 account statements export your complete trade history -- entry, exit, profit and loss per position, and commissions -- in a few clicks from the account history tab. That is the core document your tax return is built from.

Withdrawals process in under 12 minutes on average with zero fees, so moving your tax set-aside out of the trading account the day you take profits is straightforward.

$3/side commission on ECN accounts appears as a separate line item in every trade confirmation, making your deductible costs easy to isolate.

Condition | Detail |

|---|---|

Minimum deposit | $10 |

Spreads | From 0.0 pips |

Commission | $3 per side ($6 round-trip per standard lot) |

Execution | STP/ECN, no dealing desk |

Platform | MetaTrader 5 (MT5), iOS and Android |

Forex pairs | 41 pairs (majors, minors, exotics) |

Average withdrawal time | Under 12 minutes |

Deposit and withdrawal fees | Zero |

Demo account | Free, unlimited, live spreads, no time limit |

Open a free demo account to get familiar with the platform before committing real money, or open a live account from $10.

Frequently Asked Questions

Do you have to pay tax on forex trading profits in Nigeria?

Yes. Forex trading profits earned by Nigerian residents are assessable income under the Personal Income Tax Act (PITA). There is no statutory exemption for retail forex gains. The Federal Inland Revenue Service (FIRS) and state Internal Revenue Boards administer collection.

Is forex trading tax-free in Nigeria?

No. While Nigeria has no specific forex-trading tax statute, the general income provisions of PITA capture profits from trading activity. The absence of a dedicated provision is not a loophole -- FIRS applies the general trading-income rules.

How much tax do you pay on forex trading income in Nigeria?

Tax is calculated at graduated PITA rates ranging from 7% on the first NGN 300,000 of taxable income to 24% on amounts above NGN 3,200,000. The Consolidated Relief Allowance (NGN 200,000 or 1% of gross income, plus 20% of gross income) reduces your taxable base before the bands are applied. The effective rate for most retail traders falls well below the headline 24%.

How do I declare forex profits to FIRS?

File an annual self-assessment return with your state Internal Revenue Board (or FIRS if you are in the FCT) by 31 March of the following tax year. Report net forex profit as trading income. You will need a full broker account statement, a naira conversion of each trade at the CBN rate, and receipts for any deductible expenses such as commissions.

Can I deduct forex trading losses against my other income in Nigeria?

Not directly. Under PITA, trading losses can be carried forward and set against future profits from the same trade, but they cannot be offset against unrelated income such as a salary in the same tax year. Capital losses under the Capital Gains Tax Act are separately ring-fenced.

Does Nigeria have capital gains tax on forex trading?

Nigeria levies Capital Gains Tax at 10% on disposal of chargeable assets, but spot forex trading profits are generally treated as trading income under PITA rather than as capital gains. The distinction matters because trading income is taxed at progressive rates and losses are treated differently.

What records do I need to keep as a forex trader for Nigerian tax purposes?

Keep your full broker trade history, bank statements, and all expense receipts for at least six years. Convert each trade's profit or loss to Nigerian naira using the CBN official rate on the closing date. A simple spreadsheet recording date, currency pair, profit or loss in foreign currency, CBN rate, and naira equivalent is sufficient for most retail traders.

Are forex profits from offshore brokers treated differently in Nigeria?

No. Nigerian tax law taxes residents on their worldwide income. Profits earned through an offshore broker, whether held in a foreign currency account or repatriated to Nigeria, remain taxable. Retaining profits offshore does not defer or eliminate the Nigerian tax obligation. For a comparison of how a neighbouring jurisdiction handles the same question, see forex trading tax in South Africa.

What happens if I do not declare forex income to FIRS?

FIRS can assess unpaid tax at any time within six years of the relevant assessment year, or at any time if fraud or deliberate omission is involved. Penalties include 10% of the unpaid tax, interest at the CBN rate, and in serious cases, prosecution under the FIRS Establishment Act 2007. Voluntary disclosure before an investigation begins typically results in reduced penalties.

Risk warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. Consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. Past performance is not indicative of future results. This article is for informational purposes only and does not constitute financial, investment, or tax advice. Tax outcomes depend on individual circumstances and legislation changes. Consult a registered Nigerian tax practitioner before making any decisions.